HBCU borrowers question little loan forgiveness, delays to financial security

By Charlene Crowell

Although a college education is strongly believed to be the bridge to a better life, building financial security is a long way off for millions of graduates beginning their careers with heavy student loan debt. Fortunately, a near two-year pause on federal student loan payments has enabled many borrowers to diminish other debts in the interim. But the amount of time it will take to eliminate the combined $1.6 trillion of student loan debt weighs heavily on the nation’s 44 million borrowers.

New research by the Center for Responsible Lending (CRL) finds that the disproportionate level of debt incurred by students at Historically Black Colleges and Universities (HBCUs) is delaying the pursuit of wealth-building options, despite federal programs specifically designed to ensure that student loan repayment will not be akin to a 30-year mortgage.

“HBCU students receive less institutional aid and are more likely to take out loans than their peers at non-HBCU institutions,” said Christelle Bamona, researcher at CRL and co-author of the report. “While President Biden’s recent historic student loan relief plan will benefit millions of federal student loan borrowers, including HBCU borrowers, policymakers must now work to reverse the systemic underfunding of HBCUs and increase the purchasing power of the Pell Grant, among other reformative measures.”

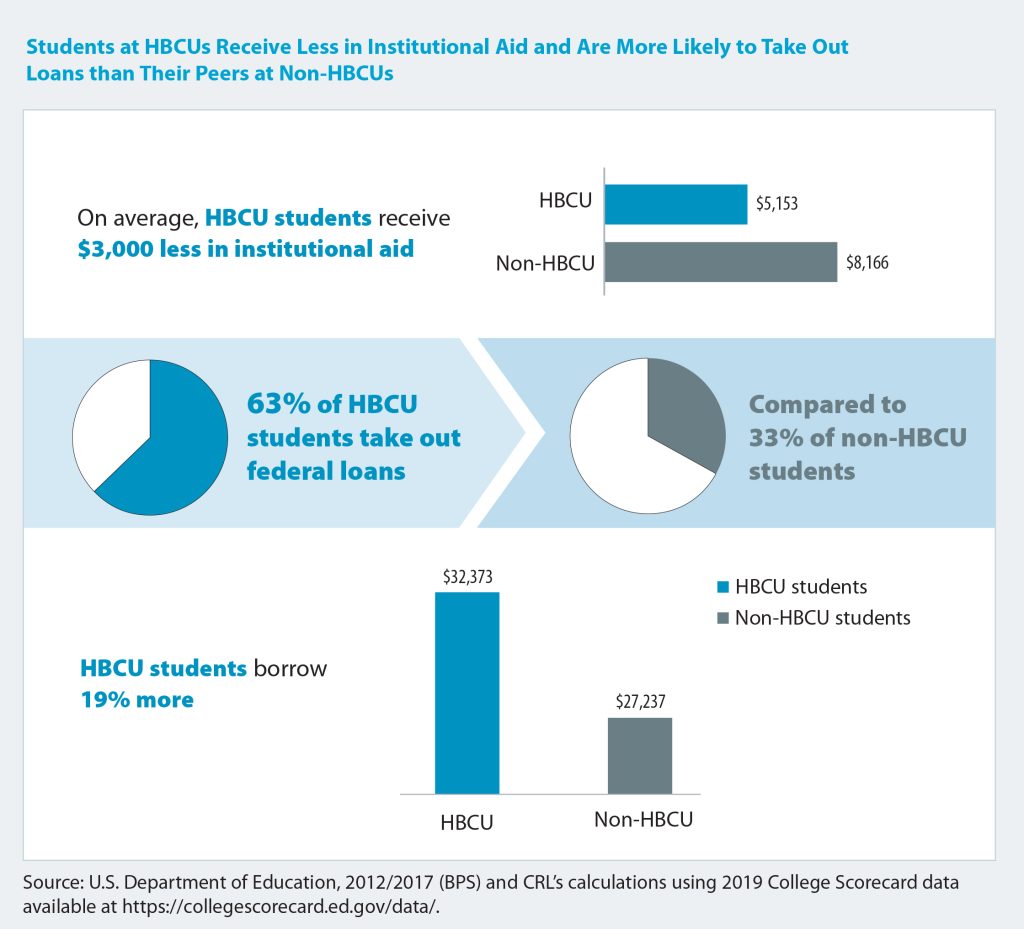

To capture this stark financial dilemma, CRL utilized a combination of data analysis and focus groups comprised of HBCU borrowers that together depict how nationwide HBCU attendees and alumni collectively owe a record $40 billion dollars in student debt, with an average debt load at graduation of $32,373 – 19 percent higher than their peers at non-HBCU institutions. This research was completed prior to President Biden’s announcement of loan forgiveness.

To capture this stark financial dilemma, CRL utilized a combination of data analysis and focus groups comprised of HBCU borrowers that together depict how nationwide HBCU attendees and alumni collectively owe a record $40 billion dollars in student debt, with an average debt load at graduation of $32,373 – 19 percent higher than their peers at non-HBCU institutions. This research was completed prior to President Biden’s announcement of loan forgiveness.

According to the new report, Paying from the Grave, among the nearly 280,000 HBCU students enrolled in more than 100 institutions, 70 percent are eligible for Pell Grants. Although the maximum $6,500 Pell Grant has remained the same since 1980, the percentage of its actual financial assistance shrinks with every passing year due to decades of rising college costs.

For example, during the 2019–2020 academic year, the average Pell grant was only $4,491 while the average tuition, fees, room, and board at a four-year institution that same year was $29,436. Due to a lack of family wealth, 60 percent of HBCU families have no means to contribute any funds at all toward a student’s college expenses.

As a result, the financial pressure to begin post-graduation loan repayment leads to 60 percent of HBCU graduates taking jobs either outside their fields of study or accepting less desirable positions. Another 37 percent of these students either delayed continuing their education or buying a home.

Gabriella, a focus group participant, shared the tough choices she faced post-graduation. Despite a dozen years of loan repayment, she still owes $100,000. As a nonprofit executive, she enrolled in the federal Public Service Loan Forgiveness (PSLF) program that affords public service employees loan forgiveness after making 120 qualifying payments. She said she felt trapped because if she were to take a job in the private sector, she could forfeit future loan forgiveness.

“I do feel even though I am passionate about the work that I do in nonprofit, I almost feel like I have to work in nonprofit in order to make sure that my student loans get paid off,” said Gabriella. “So, my career choices are limited. And even when I look for other jobs, I’m always trying to make sure [that] they qualify for PSLF …So I do kind of feel trapped in a sense to making specific types of professional decisions because of PSLF.”

Receiving PSLF loan forgiveness has been a daunting effort for all students. According to CRL’s report, between November 2020 and July 2022, the Department of Education approved only two percent of PSLF forgiveness submissions. HBCU alumni contend and public enforcement actions show that student loan servicing errors are a significant contributor to the program’s failures.

The encouraging news from the report is that the extended payment pause provided HBCU graduates much-needed relief and the opportunity to reduce debts.

“Our research also showed that the payment pause played an important role in borrowers’ finances and mental health,” said Lucia Constantine, a CRL researcher and report co-author. “The payment pause enabled 85 percent of HBCU students to make at least one positive, wealth-promoting financial choice, such as starting or building emergency savings and paying other debts. Borrowers also reported being better positioned to achieve long-term goals like homeownership, pursuing further education, or starting a business.”

CRL’s report offers multiple recommendations to lighten the load of student debt, including holding predatory student loan servicers accountable and doubling the Pell Grant program. Additionally, CRL calls for larger and sustained investments in HBCUs to increase grants and scholarships that would diminish the need for high-cost borrowing.

As the report states, “Taking on a large debt at an early age impacts lifetime earnings and generational wealth by delaying or preventing the opportunity to buy a home, start a business, or invest in retirement, thereby widening the racial wealth gap.”

Charlene Crowell is a senior fellow with the Center for Responsible Lending. She can be reached at Charlene.crowell@responsiblelending.org.